What is Fintech?

When people hear the term fintech, a few common questions pop up: What exactly is it? How does it help us? How can we benefit from it?

Fintech, short for financial technology, is where finance meets innovation. It’s the use of technology such as apps, software, and digital platforms to make financial services faster, easier, and more accessible.

Examples include:

- Mobile banking apps

- Online payment systems (like PayPal, JazzCash, Easypaisa)

- Investment apps

- Digital lending platforms

Financial Inclusion Gap in Pakistan

Despite progress, Pakistan continues to face a significant financial inclusion gap. According to the World Bank’s Global Findex, only around 21% of adults have a formal bank account. This means most rely on cash transactions, limiting access to formal credit, savings, and secure payment channels.

However, this landscape is changing rapidly. Pakistan’s fintech sector is being fueled by innovation, widespread smartphone adoption, and expanding internet connectivity. With a population of over 240 million, the country is aiming for 75% adult financial inclusion by 2028 (up from 64% today).

Supportive State Bank of Pakistan (SBP) regulations and a growing startup ecosystem have made Pakistan an emerging fintech hub.

From a Cash-Heavy to a Cash-Less Economy?

Pakistan has long been a cash-driven economy, with 85% of all transactions still done in cash. Even though cash use at Point-of-Sale (POS) terminals dropped from 84% in 2019 to 78% in 2023 (Statista), the informal sector still accounts for over 40% of GDP.

Recently, small but important shifts are happening:

- Taxi drivers, shopkeepers, and small vendors are adopting digital wallets

- E-commerce and service platforms are expanding online payment options

Benefits:

- Individuals: More convenience, security, and faster transactions without carrying cash

- Small businesses: Wider customer reach, better record-keeping, and improved transaction transparency

- National economy: Increased financial inclusion, reduced informal sector, and stronger regulatory oversight

Funding Mechanisms for Fintech in Pakistan

Pakistan’s fintech funding ecosystem is still developing, but multiple channels exist:

- Bootstrapping (founders’ own capital)

- Angel investors (early-stage capital)

- Venture capital (growth-stage funding)

- Accelerator programs (mentorship + funding)

- Government schemes such as the Pakistan Startup Fund (PSF) and Ignite

- Crowdfunding platforms and microfinance institutions

- Donor agencies that fund high-risk early-stage projects until larger investors step in

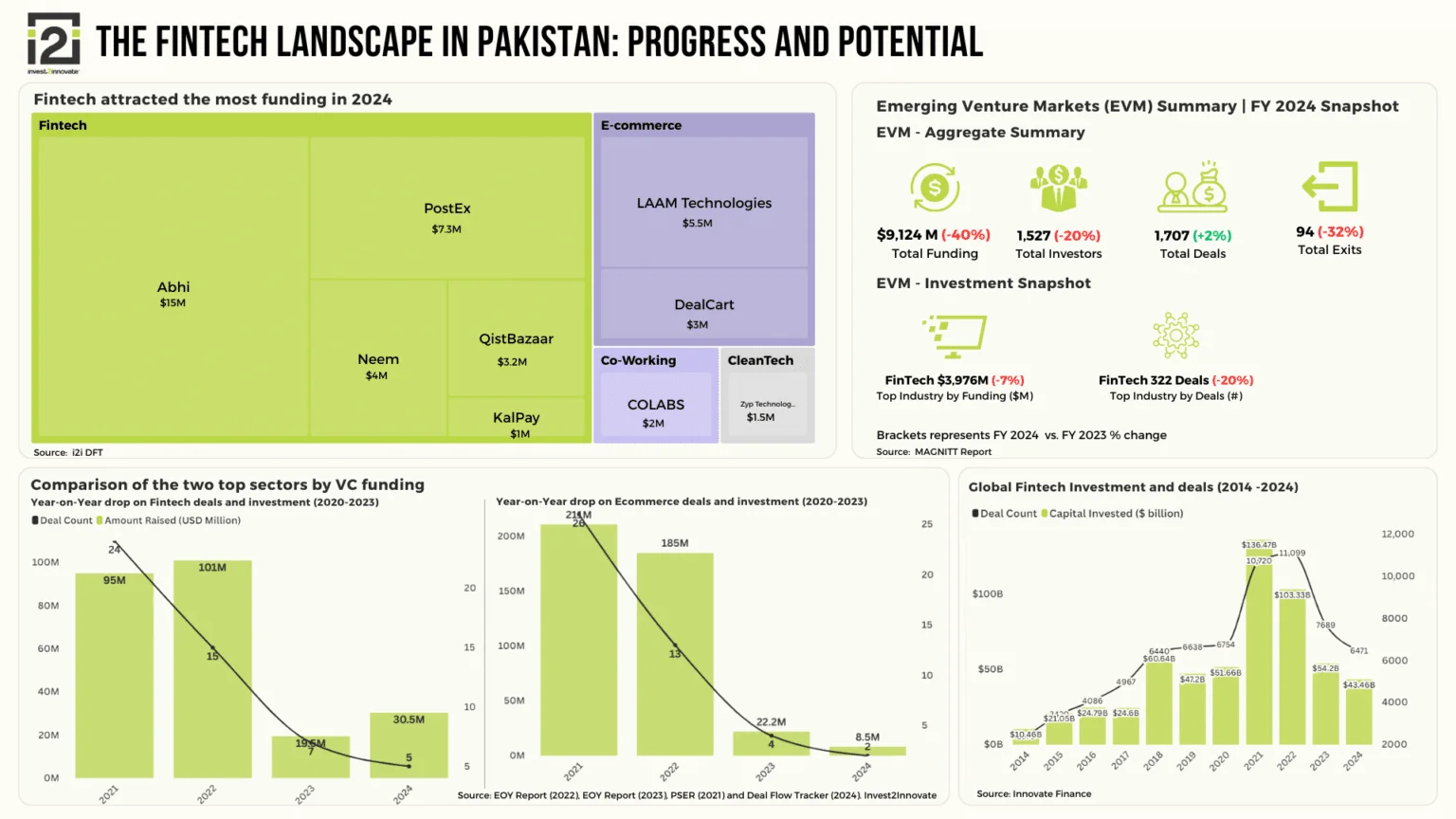

Source: https://invest2innovate.com/the-fintech-landscape-in-pakistan-progress-and-potential/

Case Study: JazzCash Scaling Financial Inclusion Through Mobile Banking

1. Origin & Market Gap

- Launched: 2012 as MobiCash (partnership between Mobilink & Waseela Microfinance Bank)

- Market gap: Like Easypaisa’s early phase, Pakistan’s unbanked population needed low-cost, accessible financial services

- Opportunity: Leveraged Mobilink’s massive telecom base (50M+ users) to scale quickly

2. Strategic Positioning

- Focused on speed, convenience, and reliability not just being another payment platform

- Positioned itself as a digital lifestyle enabler

3. Unique Selling Points

- Distribution advantage: Mobilink’s retail network allowed rapid agent onboarding

- Brand trust: Backed by Pakistan’s largest telecom

- Early traction: Millions of active wallets and agent locations within a few years

4. Milestones

- Partnered with NADRA for biometric verification

- Integrated with e-commerce platforms for seamless payments

- Reached 50M+ registered users by 2021

5. Pitch Evolution

- Started as a cash-in/cash-out service for rural customers

- Evolved into a complete fintech ecosystem mobile wallets, bill payments, government disbursements, QR payments, international remittances

- Incorporated financial literacy as part of its brand story

6. Lessons for Founders

- Leverage existing assets for rapid growth

- Continuously innovate beyond your initial product

- Show clear metrics to investors for credibility

How Startups Drive Fintech in Pakistan

Emerging startups are plugging gaps left by traditional banking. They deliver:

- User-friendly apps and digital wallets

- Real-time payment platforms for underbanked communities

- Creative models like Buy Now, Pay Later (BNPL), gig worker microfinancing, and e-commerce integration

These startups can pivot quickly, meet customer needs fast, and partner with banks or telecoms to accelerate adoption.

Opportunities and Growth Drivers

Pakistan is becoming one of the most promising fintech markets in Asia because of:

- High mobile and internet penetration even in rural areas

- SBP’s Raast instant payment system

- Young, tech-savvy population (64% under 30) ready to adopt digital finance

- Rising success stories like Easypaisa, JazzCash, Sadapay, NayaPay, and Abhi

What’s Next?

The future holds exciting possibilities:

- Islamic fintech solutions

- AI-based credit scoring

- Open banking frameworks

- Cross-border digital payments

If government, regulators, and private investors collaborate, Pakistan’s fintech sector could become a regional leader in digital finance

FAQ

Fintech uses digital tools to make finance more accessible. In Pakistan, it addresses the low bank account penetration and dependence on cash.

From bootstrapping and angel investors to venture capital, accelerators, crowdfunding, and government programs like PSF and Ignite.

Islamic fintech, AI-driven credit systems, open banking, and cross-border payments.