The $36.6 million raised in 2025 tells a deeper story not of recovery, but of an ecosystem learning where resilience truly lies.

In 2025, Pakistan’s startup ecosystem showed signs of stabilization after multiple years of contraction. According to a newly released snapshot by Data Darbar, disclosed equity funding for startups rose to $36.6 million, a notable improvement compared to the depressed totals of the immediate prior years.

This article examines the data, underlying dynamics, structural stresses, investor psychology, sector trends, gender participation, and future outlook for Pakistan’s nascent yet strategically significant startup ecosystem.

1. Funding Overview and Deal Activity

- Total disclosed equity funding reached $36.6 million during 2025.

- There were 14 disclosed equity transactions, though only 10 of these included public funding figures, indicating continued investor caution at early stages.

These figures represent a modest rebound from the low base of the prior three years, during which funding volumes and deal counts had contracted significantly due to macroeconomic pressures and risk‑averse investor behavior.

Investor Behavior Insight:

The fact that fewer rounds disclosed amounts suggests that investors and founders alike are selectively transparent, possibly aiming to avoid market signaling that could influence valuation expectations or negotiations. This reflects evolving deal conventions in an immature capital market.

| Year | Total Funding ($M) | Number of Deals |

| 2023 | 28.5 | 18 |

| 2024 | 32.0 | 16 |

| 2025 | 36.6 | 14 |

2. Sectoral Funding Distribution

The concentration of funding provides insight into investor confidence and perceived scalability:

Fintech – The Dominant Sector

- Fintech continued to capture the largest share of funding and deal activity.

- Haball’s Pre‑Series A round stood out as one of the year’s largest equity injections, supported by institutional capital.

- Other fintech players, like Metric, raised substantial seed funding (~$1.3 million), particularly in B2B financial infrastructure.

Pakistan’s fintech sector is seen as less dependent on discretionary consumer spending and more grounded in enabling financial infrastructure making it attractive in an economic environment marked by volatility. This aligns with broader regional signals of fintech adoption, where digital finance is expanding despite structural limitations in traditional banking penetration.

Healthtech – Rising Momentum

- Healthtech emerged as the second strongest sector, spearheaded by MediQ’s $6 million Series A among the largest disclosed deals.

- Early‑stage health startups also attracted investment focused on digital care delivery, diagnostics, and wellness solutions.

Investors see healthtech as mission‑aligned with pressing demographic needs and capable of building reliable, recurring revenue through essential service delivery.

Other Sectors: Commerce, Logistics, SaaS

- Outside the leading categories, startup funding remained modest and largely concentrated at the seed and angel levels.

- These sectors reflect experimentation rather than robust capital commitments, highlighting the need for stronger business models to attract sizable investment.

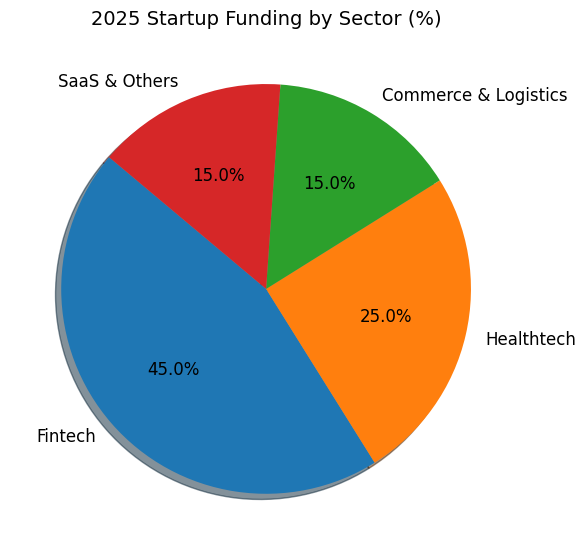

Distribution of disclosed startup funding in Pakistan for 2025, highlighting sectoral dominance. Fintech attracted the largest share (45%), followed by Healthtech (25%), with Commerce & Logistics and SaaS & Others each receiving 15%. This distribution reflects investor confidence in financial infrastructure and digital health solutions amid economic uncertainty.

3. Gender Dynamics and Diversity

One of the most promising signals from the 2025 data was an improvement in funding for female‑led startups:

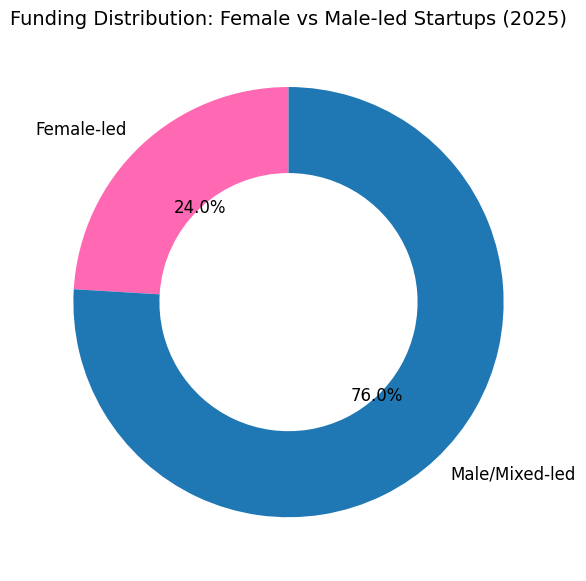

- Female‑led teams raised ~$8.8 million, accounting for nearly 25 percent of disclosed equity.

While this share appears significant, analysts caution that percent gains are amplified by the relatively low overall funding base. Nonetheless, this shift suggests incremental progress in a historically male‑dominated investment landscape and should be monitored as a leading indicator of broader inclusion.

Equity funding distribution between female-led and male/mixed-led startups in 2025. Female-led teams accounted for 25% of disclosed funding (~$8.8M), signaling gradual progress toward gender inclusion in a historically male-dominated entrepreneurial ecosystem.

4. Investor Strategy and Ecosystem Psychology

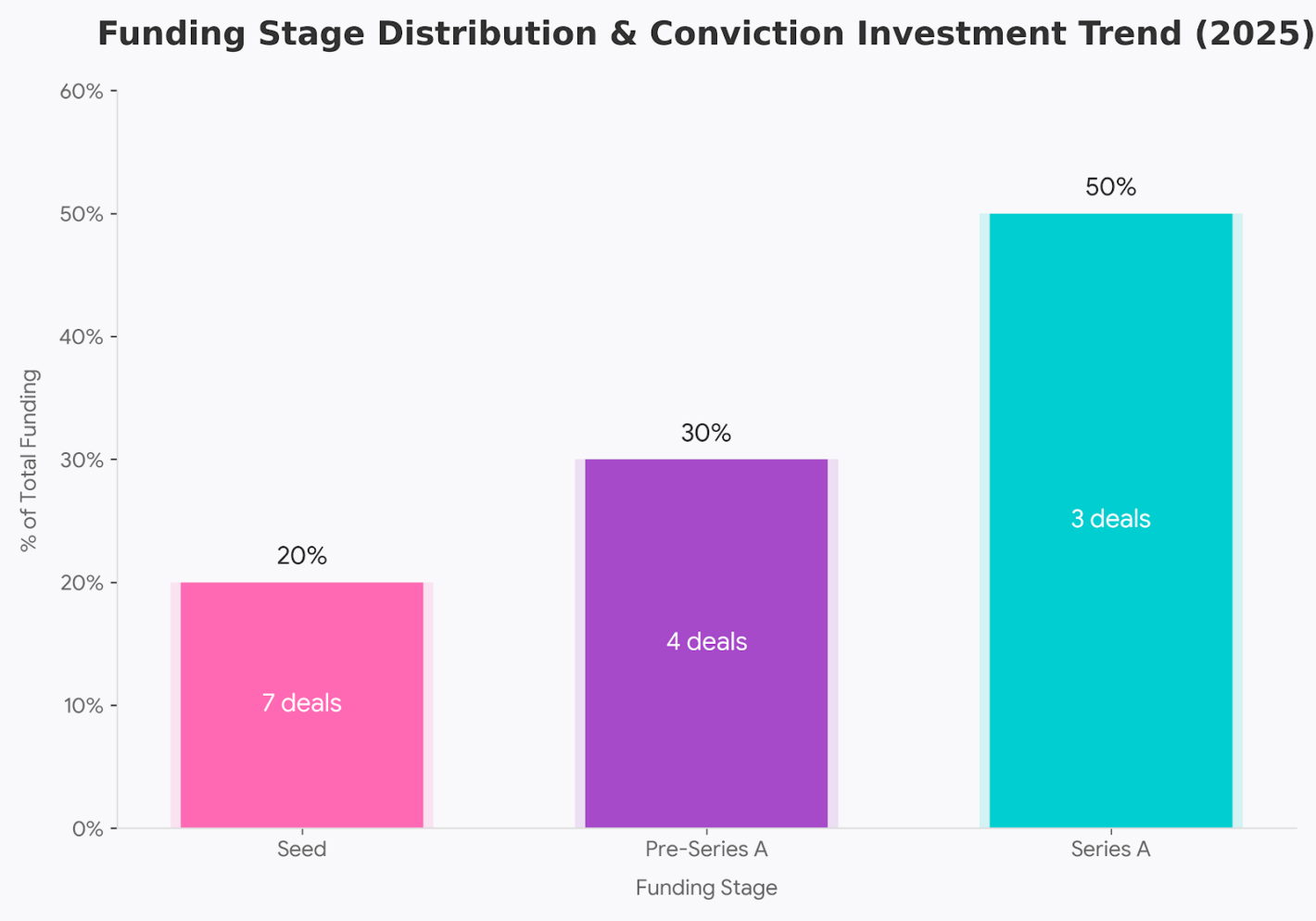

Fewer Deals, Larger Convictions

One discernible trend is a shift from numerous small seed deals toward fewer, larger, conviction‑based investments. This strategy reflects:

- Heightened selectivity among VCs and angel investors.

- Prioritization of startups with proven unit economics or revenue paths.

- A risk‑mitigated approach amid macroeconomic uncertainty and currency volatility.

This risk posture is not unique to Pakistan’s market. Globally, venture funds have pulled back from broad early‑stage portfolios in favor of backing resilient, revenue‑oriented businesses.

Quality over quantity: 50% of capital is now fueling the top tier of high-conviction Series A deals.

Alternative Financing Emergence

There is evidence of increasing reliance on non‑traditional capital sources, such as:

- Venture debt

- Strategic partnerships

- Structured financing mechanisms

These approaches help founders stretch equity runway and reduce dilution, signaling maturing entrepreneurial finance strategies.

5. Structural and Market Constraints

While 2025 presents green shoots, challenges persist:

Broader Economic Headwinds

Pakistan’s macroeconomic pressures high inflation, currency stress, and constrained liquidity have historically dampened risk capital inflows. This has translated into:

- Reduced deal counts

- Slower early‑stage funding commitments

- Greater emphasis on capital efficiency

These factors have shaped investor risk appetites and founder strategies, forcing startups to manage cash flows meticulously.

Market Depth & Local Capital Participation

A long‑standing challenge remains limited participation from domestic institutional capital. Many earlier ecosystem analyses underscore that a large share of venture capital historically came from foreign sources, with local family offices and institutional investors yet to scale their involvement meaningfully.

Expanding domestic investor engagement is critical for sustainable ecosystem growth.

6. Outlook and Strategic Imperatives

Stabilization with Caution

The 2025 funding figures suggest a stabilizing startup ecosystem, one that is:

- Recovering from contraction.

- Leaning toward concentrated investments.

- Fostering sectors with tangible product‑market fit.

Strategic Recommendations for Stakeholders

- Founders: Prioritize clear monetization pathways and operational discipline to attract conviction funding.

- Investors: Balance portfolio diversification with deep due diligence and stage‑appropriate support.

- Policymakers: Encourage local institutional participation and strengthen regulatory frameworks that enable venture capital growth.

7. Conclusion

The Data Darbar 2025 funding snapshot, while modest in absolute terms, represents a critical inflection point. It signals a shift from survival mode to selective confidence among investors and a maturing ecosystem increasingly capable of weathering structural headwinds.

Pakistan’s startup landscape remains young, and its trajectory will depend on sustained investor interest, domestic capital activation, and sector‑specific value creation strategies. Continued tracking of funding patterns, gender participation, and alternative financing mechanisms will be essential for understanding how the ecosystem evolves in the years ahead.